Author: Teddy DeWitt, PhD, Lead Computational Social Scientist

Recession Fears Linger Amidst Consumer Pessimism and Tariff Uncertainty

The U.S. economy may be showing signs of fatigue. The Conference Board Leading Economic Index fell for the sixth straight month in May, suggesting a slowdown in American economic activity. In the wake of ongoing tariff pressures, the University of Michigan’s Index of Consumer Sentiment reached its second lowest level of all time at 52.2 in April of this year. While the measure rebounded in June, it is still down 11% year over year. Given these factors, plus the rise in geopolitical tensions with the Israeli and American attacks on targets in Iran, and Iran’s retaliatory threat to block the Strait of Hormuz, a major shipping lane for crude oil, recession fears are on the minds of many.

At interos.ai, understanding and measuring recession risk is a key part of our process for evaluating financial risk at the country level. Specifically, we developed our Recession Warning Indicator to provide a forward-leaning barometer of future economic instability within a country.

We looked at financial risk from the “Liberation Day” announcement in April to assess financial anomalies and lurking risks – covering a deeper view of the financial fallout in our Tariffs Report. Our analysis, based on our Recession Warning Indicator and follow-on research, suggests that while the world economy is currently avoiding recession, many countries are still at high levels of risk. This indicator is a key risk factor that interos.ai tracks as we understand that recession risk in one country can ripple through trade partners. This ripple effect can lead to weakened export markets, decreased investor sentiment and overall destabilized global supply chains. A combination of ongoing geopolitical events and tariff headwinds could shift some of those countries into recession this year.

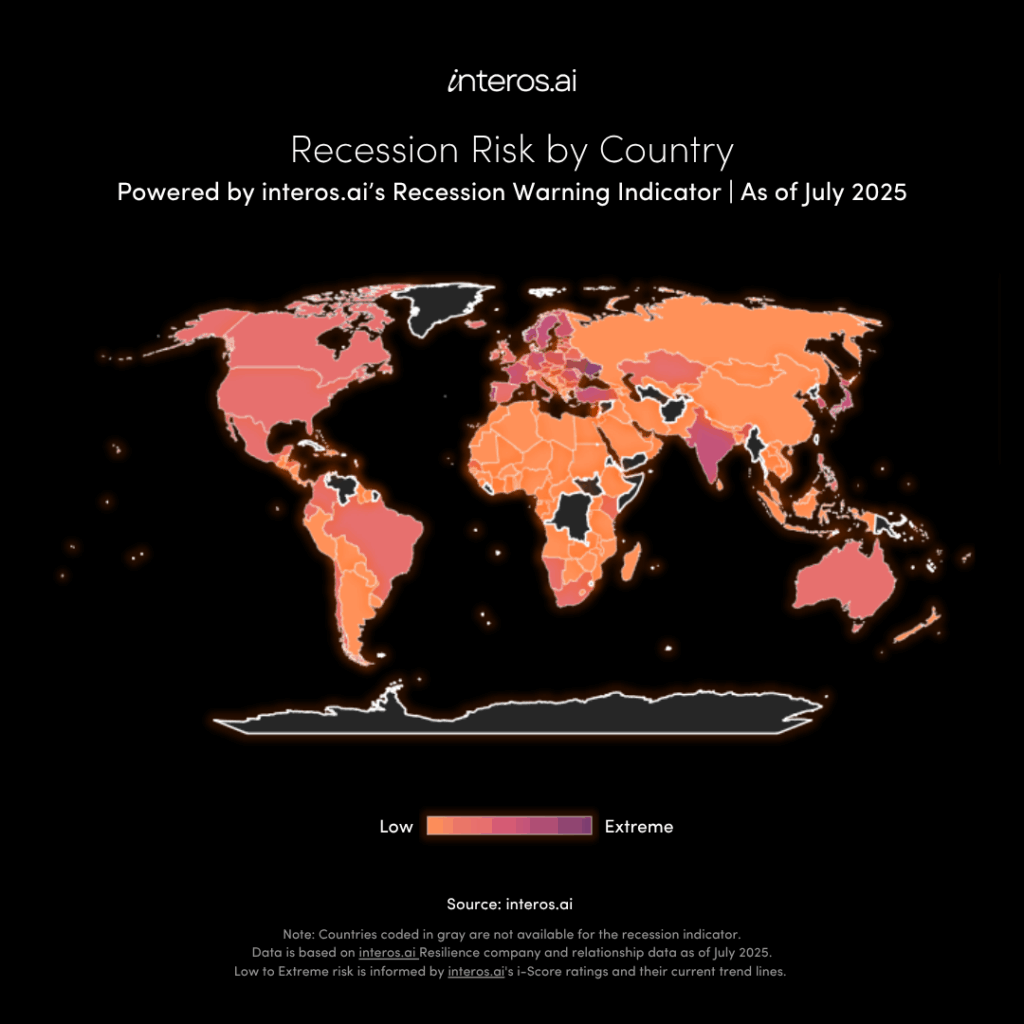

Assessing Recession Risk: interos.ai Highlights Three Global Trends

interos.ai’s Recession Warning Indicator helps identify countries that are at risk of recession in the near future. This indicator assesses trends across major economic signals including GDP growth rates, unemployment rates, inflation rates and consumer spending metrics. Our computational methods combine these trends into a score with the same risk categories as set out in our broader i-Score™ methodology. This metric allows us to assess:

- As the concern for a potential recession increases for the American economy, is the U.S. an isolated case or part of a more widespread pattern?

- Compared to historical trends, is the recession risk increasing or decreasing?

The interos.ai Recession Warning Indicator highlights three global trends:

1. Europe and the Eurozone broadly are at the greatest risk of recession.

Globally, there are 54 countries with a Recession Warning indicator falling within the high-risk category. Of these, 38 countries are in Europe. This finding is consistent with the overall projection of modest growth for the region, with the European Commission projecting GDP growth of 1.1%, and the European Central Bank seeing slightly more tepid growth at 0.9% actions taken by the European Central Bank who cut short term interest rates in June for the 8th time this year to 2%. A recession in this massive trading area would greatly impact the global economy.

2. North America may not be far behind Europe: high recession risk looms.

The U.S., Canada and Mexico all have scores within the high-risk category. However, these scores are overall improvements from October of last year when the scores for these countries were nearly 38% lower and subsequently deeper into the high-risk zone. This improvement represents outperformance compared to the global median percentage increase coming in at 27% over the same period. Nevertheless, the uncertainty around tariffs is the primary concern for North America broadly and the United States specifically. The ultimate size of tariffs has the potential to dramatically impact GDP in the second half of the year. According to some economic forecasters, the simple lack of clarity around what the tariff regime will look like, could significantly hinder economic growth and stability. U.S.-based companies will face impacts not just at home, but across their global supply chains, compounding existing vulnerabilities and triggering widespread disruptions.

3. The picture for Asia is a mixture of vulnerability and strength.

Three of the largest economies in Asia: Japan, Korea, and India, all are within the high risk category of the Recession Warning indicator. However, China, Vietnam, Singapore and Thailand are safely in the moderate risk category trending towards low risk.

Despite China being low risk, the country alone makes up nearly 20% of the world’s global GDP which means a recession would devastate global supply chains. Vietnam’s economic growth story is particularly interesting as it experienced GDP growth of 7% in 2024, partially grounded in reshoring trends as much as 8% in 2025 until tariff uncertainty creates some economic headwinds. That said, Vietnam’s economic growth story remains strong with GDP growth forecasts of 6.8% for 2025, anticipated from a combination of strength in manufacturing and tourism. Additionally, Trump has struck a preliminary deal with Vietnam that would drop tariffs from 46% to 20%, which makes it a more attractive market for longer term stability. However, even though it is a lower risk market, companies still need to assess potential suppliers on all six risk factors spanning cybersecurity, geopolitical, ESG, extreme weather, restrictions and financial risk.

Anticipate and Adapt: What’s Next For Your Supply Chain?

In the coming months, there are several global factors to watch that will have a large impact on the global economy.

- Whither Tariffs? – While the Trump Administration’s willingness to delay on enacting its trade policy has resulted in positive reactions from financial markets, a lack of executed trade deals with our largest trade partners gives ongoing reason for caution. However, the recent additional tariffs on Mexico and the EU as well as 23 other trading partners paint a volatile landscape and set the stage for retaliatory measures. Retaliatory tariffs from China along with its export controls on critical materials like rare earth minerals are an example of the risks created by tariff policies. These factors will continue to percolate through the American economy and beyond, leaving many companies struggling to avoid unexpected financial challenges and supply chain disruptions.

- Iranian Blockade of the Strait of Hormuz – By some estimates, 20% of global crude oil shipments flow through this passageway. Crude oil importers such as China and Japan could take an economic hit in the event of a prolonged blockade. In the case of Japan, this could either maintain or add to its potential economic weakness. A blockade of this vital area would cause spikes in energy prices leading to increased transportation and manufacturing costs.

- Ongoing Global Conflict – With the Ukraine/Russia conflict persisting, we can expect the resultant humanitarian crisis and supply chain interruptions to continue to weigh on Europe’s economy. Given the possibility of an expanded conflict in the Middle East due to military action by the U.S., Israel, and Iran, as well as the ever-present threat Taiwan faces from China, there is enough geopolitical tension to slow down global supply chains well into 2026 as it disrupts production and blocks trade routes, leading to longer lead times and increased costs.

As the ongoing complexity between economic policy and geopolitical events continues to play out over the coming months, the interos.ai Recession Warning Indicator will surface the areas of weakness and pockets of strength throughout the global economy.

Download our exclusive Tariffs Report for immediate insights into the evolving global supply chain landscape and what actions to take today to get ahead of supply chain shocks.