Authors: Andrea Little Limbago, Mackenzie Clark, and Theodore DeWitt

China’s exports to the U.S. dropped 25% from the same month last year. Those calling this an unexpected shift have not been paying attention. Almost a decade into a trade war that has seen thousands of companies added to various restrictions lists and tariff fluctuations including some that reached 145%, it would be more surprising if the escalating tensions did not have an impact. But that is not the whole story. There is a broader shift in China’s trade flows underway signifying a global realignment. In addition, China’s domestic economic situation often is overlooked or marginalized in many forecasts. With a global economy experiencing generational transformations, a holistic view behind the data is critical to understanding the factors behind the deltas which, in turn, are foundational for making the most informed supply chain decisions.

China’s Global Trade Realignment

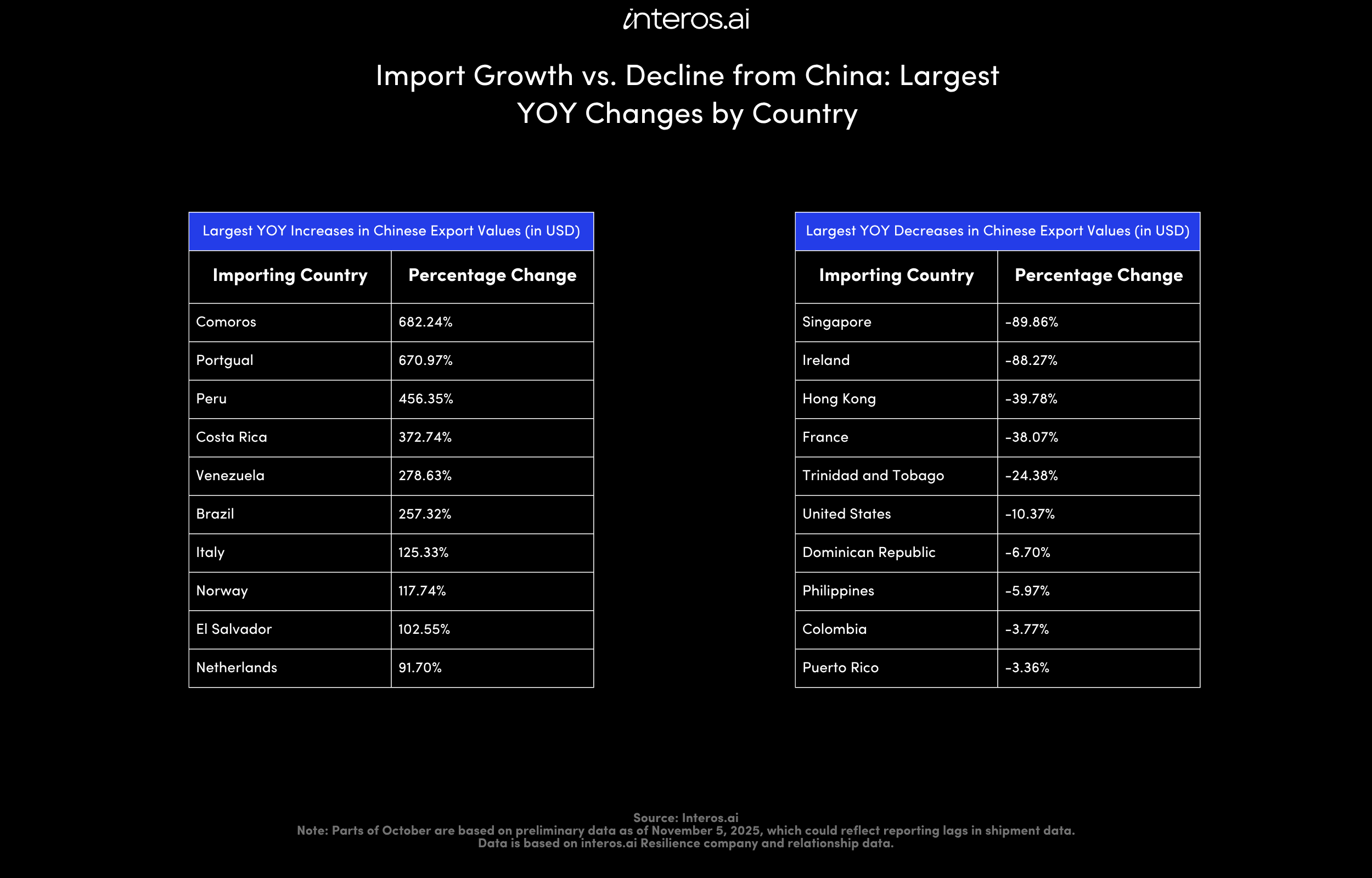

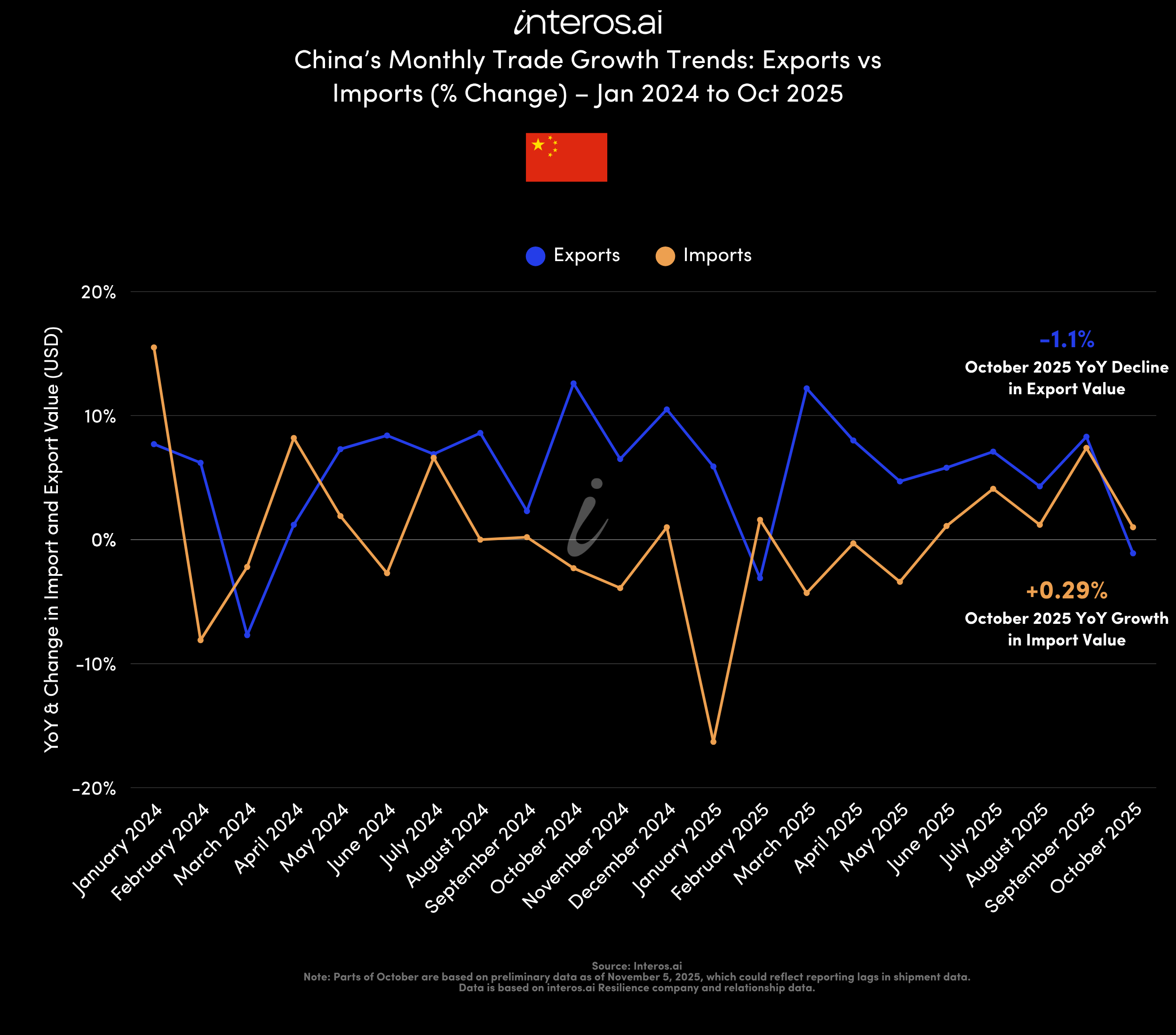

China’s exports to the US dropped 25% in October 2025 compared to October 2024. At the same time, China’s overall drop in exports was 1.1%, indicating significant restructuring globally and an increase to other countries. Economists had been forecasting a 3.1% increase. For some countries, the increase is much more dramatic. An interos.ai data analysis surfaces trends in China’s export shipment values year-over-year (in USD) for shipments between January and August. Some countries are seeing as much as a 680% increase in imports from China, while the United States is seeing over a 10% decrease YOY. The story remains the same when expanding the time frame from January to October, but due to reporting lags from some countries, the most exhaustive and reliable coverage ends in August 2025.

Several of these annual increases could be attributed to China’s ongoing efforts to expand their influence and partnership with Latin America and the Caribbean, with CELAC member states like Brazil, El Salvador, Peru, Costa Rica, and Venezuela among the countries with the highest YOY increases in Chinese export values. In recent weeks, China also expanded trade agreements with ASEAN countries. China continues to grow these regional partnerships, which may prove to be a key strategy to ensure economic growth, especially in the face of declining US imports.

The drop in China’s exports to the US is also suppressing another key data point in geo-economic competition. China’s exports to Russia dropped 8.7% year over year in first 10 months, while Russia’s exports to China faced a 5.9% decline. These net drops in trade resulted in a loss of $184.7B and $101.2B, respectively. To add to this, China suspended purchase of Russian oil by their key oil companies, such as PetroChina, Sinopec and CNOOC. Much of this may be in response to recent US sanctions on Russian gas giants Lukoil and Rosneft, which occurs at a time when Russia’s oil revenue is plummeting. This is quite the fluctuation from the impression displayed just two months ago at the Shanghai Cooperation Organization Summit.

Looking Beneath the Surface at China’s Domestic Economy

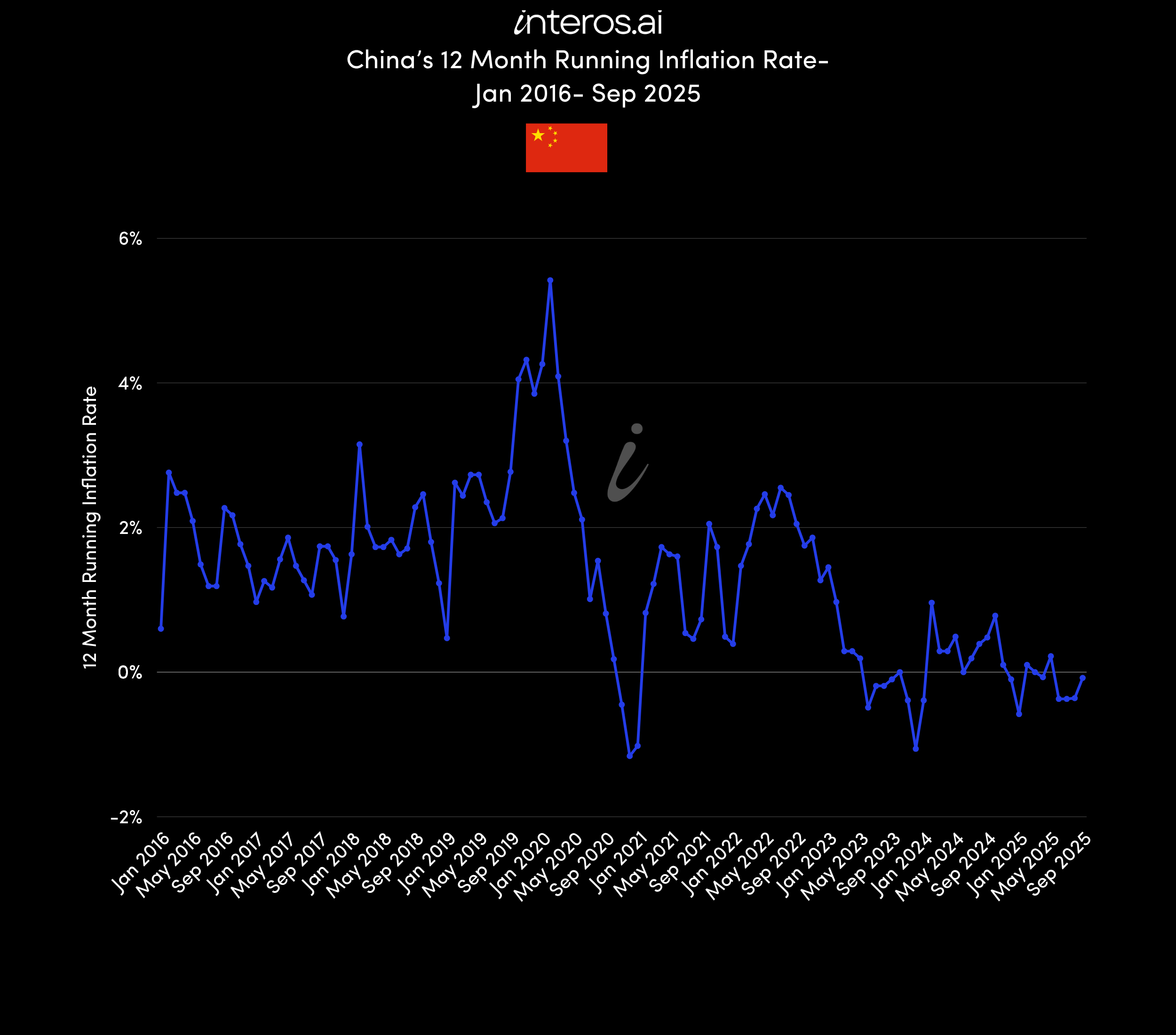

According to Barclay’s economist, Yingke Zhou, if exports are not sustained, “China’s growth could face a ‘triple whammy’ from the prolonged contraction in the property sector, and weakened private consumption and exports.” According to interos.ai data analysis, China’s economy has been deflationary since October 2024 (see chart below), with changes in the Consumer Price Index (CPI) at 0 or negative for the past year. A combination of persistent industrial overcapacity and weak consumer demand has led to increased domestic competition and price wars. These price wars are fueling the deflationary spiral, hitting industries from automotive to coffee to real estate. The price cuts required to dominate industries have the simultaneous impact of creating overcapacity and “involution” – the term used in government policy documents referring to race-to-the-bottom competition.

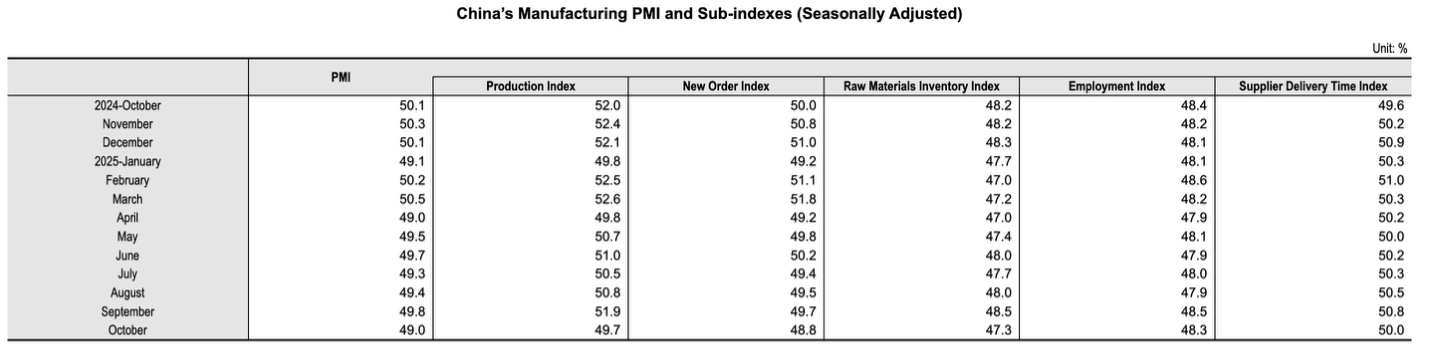

Moreover, additional, but largely unreported, preliminary release data further corroborates the domestic economic challenges underway. The Purchasing Managers’ Index (PMI) for October reveals a decline of .8%, moving it to 49%. The PMI is comprised of production, new orders, raw materials inventory, employment, and supplier delivery time indices (see the chart below). Each shows a decline and/or are hovering around 50% and reflect additional economic contraction.

Finally, there are broader trends across China’s economy worth watching. The marginal productivity of capital keeps decreasing, while consolidation is likely to continue to occur to address involution, and the real estate market remains sluggish after years of challenges. China also experienced record levels of foreign direct investment flight in 2024, with $168B fleeing the country. This all comes at a time when China is experiencing a demographic crisis at an unprecedented scale and speed. Of course, there are bright spots as well – such as a 9% increase in rare earths exports in October and global foreign trade increasing 3.6% from January to October – that signify more positive headwinds and illustrate the complexity of domestic economies.

The Data Challenge Going Forward

Looking ahead, accessing and trusting China’s economic data will only become increasingly important. Unfortunately, at a time when data is more abundant than any other time in history, China’s economic outlook and forecasts face a data gap. For instance, following the wave of media reports on the drop in exports to the US, preliminary data for October seems to be unavailable at the time of this writing (screenshot below).

Source: english.customs.gov.cn/statics/report/preliminary.html

This is not a new problem. Following the 2021 implementation of new data security laws, maritime data plunged 90% in maritime traffic data across Chinese waters. China’s vanishing data problem has only escalated in these last few years as they stopped publishing hundreds of key economic indicators. These drops coincide with decreasing trust in China’s numbers, which is infamous for its unreliability.

In a year of unprecedented global economic shifts and ongoing competition, this is the latest – but certainly not the last – indication of the significant global transformations underway. Whether the recent summit in South Korea and subsequent tariff reductions lead to a detente, or if they are temporary, will play a critical role in trade relations not only between China and the US, but China and the world. These macro-trends and deviations from expert forecasts must become part of any agile supply chain strategy. Expecting the unexpected is critical at a time when black swan events are increasingly the norm. At interos.ai, we will continue to track these shifts and contextualize them to help our customers achieve proactive supply chain adaptability.

Connect with one of our supply chain experts today to explore how intelligence-driven insights can strengthen your operations.